Live music is entering 2026 with unmistakable momentum, and festivals sit at the center of it. Live Nation reported global attendance up 14% to 44 million fans in Q2 2025, alongside over 130 million tickets sold (through July) and $7B in quarterly revenue—a clear signal that demand is not only back, but scaling.

At the same time, consumer priorities are shifting toward experiences. Bloomberg’s trends research found that 7 in 10 people would rather splurge on an experience than buy material goods, and 21–35-year-olds are 1.4x more likely to say event spending is a high priority.

Zooming out, the broader music economy is also expanding: IFPI reports global recorded music revenues hit $29.6B in 2024 (+4.8%), with paid subscribers rising to 752M (+10.6%), meaning audiences are more connected to artists, more often, across more touchpoints than ever before.

For experience leaders, the takeaway is simple: festival growth is no longer just about lineup and scale, it’s about delivering modern, connected journeys that match today’s expectations for personalization, flexibility, and seamless commerce. That’s exactly why leading organizers are moving away from rigid, legacy systems and toward experience-first platforms designed to orchestrate the entire lifecycle (discovery → purchase → onsite → loyalty) without friction.

Market Growth & Industry Scale

1. The global music festival market will exceed $24.52B by 2034

In a recent study by Global Growth Insights, the global music festival market is valued at USD 3.76 billion in 2025 and is projected to reach USD 24.52 billion by 2034, representing a rapid compound annual growth rate of 23.17%. Notably, these figures reflect direct festival market revenue and do not include the broader live entertainment economy.

Other long-term forecasts, which include premium experiences, sponsorship activations, digital extensions, and bundled travel and commerce, estimate the festival market could exceed $37 billion by 2035—underscoring how much value sits outside traditional ticketing models.

2. Festival Growth Is Being Driven by Digital Engagement (55%) and Onsite Monetization (62%)

Festival growth is being propelled by several converging forces: strong youth attendance (40%), rising sponsorship revenue (38%), and—most notably—expanding digital app engagement (55%) alongside increasing merchandise sales (62%).

At the same time, experience expectations are evolving quickly, with mobile ticketing adoption at 65%, live streaming at 58%, and AR/VR adoption at 42% signaling a more connected, hybrid future.

Sustainability is also shaping decision-making, with 48% eco-friendly practices and 45% eco-festival growth, while APAC is accelerating at 22% year-on-year, reinforcing where the next wave of expansion is likely to come from.

3. Festivals now account for over 30% of the global event tourism economy

Festivals have become one of the most powerful engines in the global travel economy. Future Market Insights projects the event tourism market will grow from $1,697.0B in 2025 to $2,585.5B by 2035, and notes that festivals will dominate with a 32.5% market share—making them the single largest category within event tourism.

Attendance & Global Reach

4. Flagship festivals regularly attract 400,000+ attendees

Festivals like Tomorrowland, SXSW, and Sziget manage city-scale crowds, international travel flows, layered programming, and thousands of vendors, staff, and partners. What was once a live music gathering has evolved into a temporary ecosystem, combining concerts, hospitality, retail, brand activations, and media production.

Large-scale destination festivals in North America—including events operating like Coachella- and Stagecoach—anchor a disproportionate share of regional revenue (more than 60% of North America’s festival wallet share) due to their ability to attract global audiences, premium sponsorships, and multi-day spend.

When attendance reaches hundreds of thousands, margin is won or lost on operations. Infrastructure, real-time data visibility, and integrated systems are no longer optional, they are critical to managing risk, scaling profitably, and delivering a seamless experience at scale.

5. “Micro-events” are the growth play — 63% of organizers say demand is rising for smaller, more intimate experiences

Boutique and curated festivals are gaining share because they deliver what modern audiences increasingly want: connection, identity, and intentionality. Eventbrite’s TRNDS 2025 report captures the shift clearly: 63% of organizers believe consumers are looking for more micro-events and intimate gatherings—a strong signal that growth is moving toward smaller formats where community and differentiation are easier to engineer.

6. More than half of festivalgoers travel over 100 miles to attend

Music festivals are no longer just local cultural event. According to recent attendance research, more than half of festivalgoers travel more than 100 miles to attend a music festival. Nearly 58% travel more than 50 miles.

The “festival trip” mindset is real and prevalent: audiences are planning travel, logistics, and spending around these experiences. For organizers and marketers, this means prioritizing seamless booking, integrated travel offers, and localized digital journeys that turn travel intent into conversion and loyalty across the entire ecosystem.

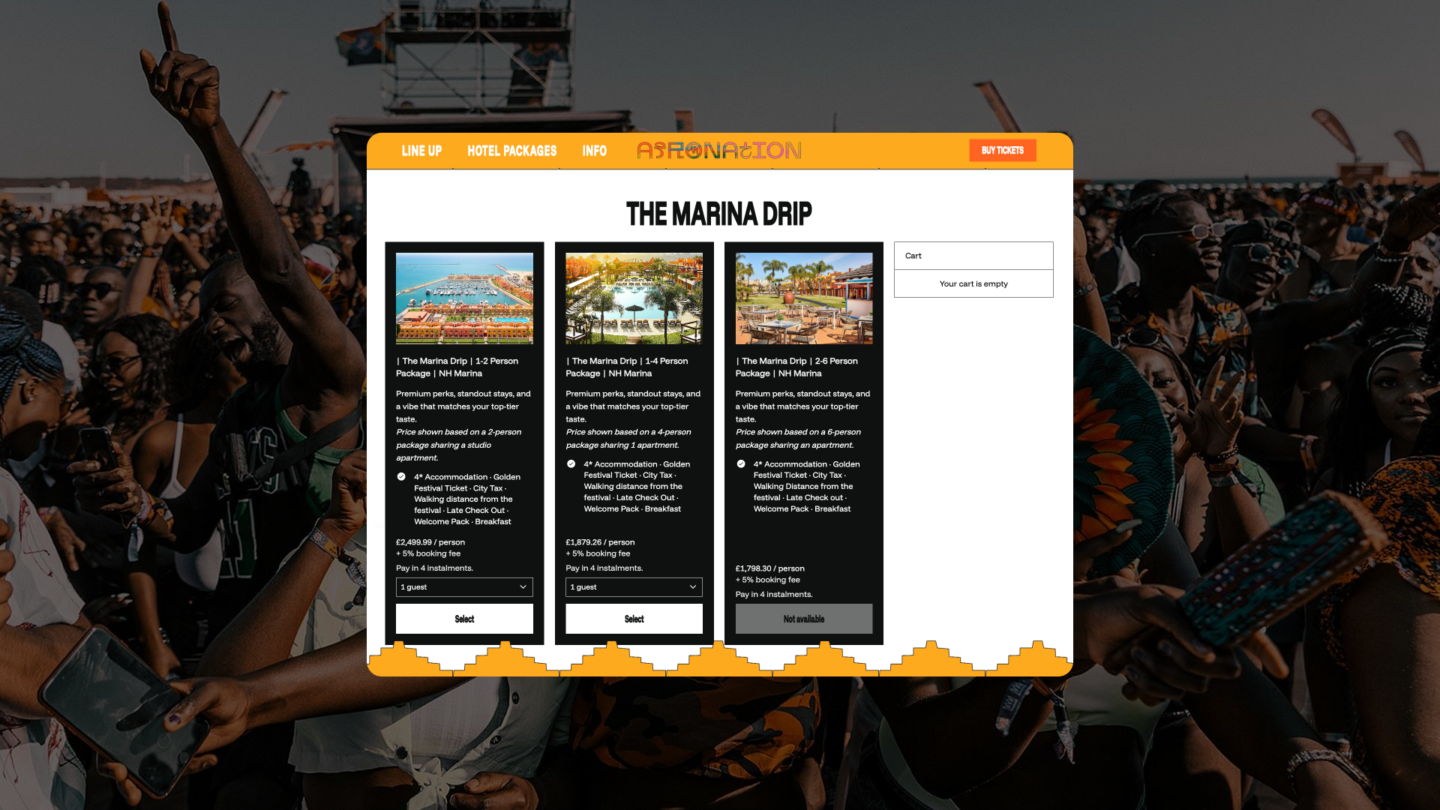

Packages: Built-In

See how Afro Nation has optimized their booking journey with built-in accommodation upsells.

Audience Demographics & Behavior

7. 18–34 year olds remain the dominant festival audience

Across the festival landscape, 18–34 year olds remain the core audience, representing approximately 60% of attendees.

This group places a premium on connection and community (what Eventbrite research has framed as the rise of “fourth spaces,” where online identity and real-world belonging converge).

They are also disproportionately digital in how they experience and market festivals—concertgoers aged 18–34 are 1.6x more likely to post about the event on social.

8. EDM festivals are growing attendance by up to 20%

Genre-specific experiences are outperforming generalist formats. At the same time, broader market data highlights explosive growth across other musical segments and regions that increasingly intersect with festival programming:

- U.S. Latin music streams up 24.1% in 2023, signaling rising demand for Latin-centric live experiences globally.

- Country music listening grew by ~23.7% in 2023, supporting expanded festival programming and regional travel demand.

- World and global genre listening (including Afrobeats and K-Pop) jumped ~26.2%

Genre diversification is expanding the festival audience and creating distinct growth pockets. While EDM remains a high-velocity segment, segments like Latin, country, and global pop are unlocking new attendance and engagement opportunities.

9. 8-in-10 organizers believe it’s important to grow communities around their events

This is a material shift in how events are built and marketed. When people feel a sense of belonging, they don’t just buy a ticket—they return, bring friends, join early-access lists, engage with content year-round, and convert into higher-value tiers.

Spending, Revenue & Monetization

10. Festivalgoers spend $60–$72 per day on food and beverage

On-site F&B is a major margin lever: Gitnux reports $60/day on food and beverages, while atVenu’s festival benchmarks show $65 per fan per day (plus ~4.2 drinks and 2.3 food items per fan per day).

11. Average merchandise spend per fan has reached ~$64

The average fan spends $64 pre-tax on merchandise in 2025 (up year-over-year), and festival benchmarks show meaningful per-fan merch spend at scale.

12. VIP and premium ticket sales have grown by ~20%

Coachella’s “Resort at Coachella” style offerings are a strong example of this done well—bundling premium accommodations with elevated festival access and on-site services (e.g., furnished lodging, VIP amenities, transport/concierge-style support).

Tomorrowland’s Global Journey is another best-in-class model: it packages festival passes + travel + accommodation + shuttles, turning a ticket into an end-to-end trip product.

Selling premium at scale usually fails when bundles are hard to assemble, price, and fulfill across systems. That’s where a packages capability matters—being able to define what’s included (inventory, entitlements, access rules), sell it cleanly, and deliver it consistently on-site.

Explore Easol Packages

Treat every guest like a VIP and enable easy booking of hotels, add-ons, and experiences, right within your native booking flow.

13. Travel and accommodation represent nearly 40% of total festival spend

Gitnux estimates 39% of total festival spending goes to travel and accommodation, reinforcing that the “festival purchase” is often a trip, not a ticket.

14. Festival ticket prices have risen ~8% annually

Festival ticket prices have increased by roughly 8% per year over the past five years, driven by higher production costs, larger lineups, expanded programming, and increased demand for premium access.

Digital Experience & Technology

15. Social media engagement spikes significantly during live festivals

Festivals are content engines as much as live events. In addition to during the event, social media also plays an important role leading up to the event. Eventbrite reported that 30% of Gen Z buyers are discovering events on TikTok, 48% on Instagram, and 24% by word of mouth.

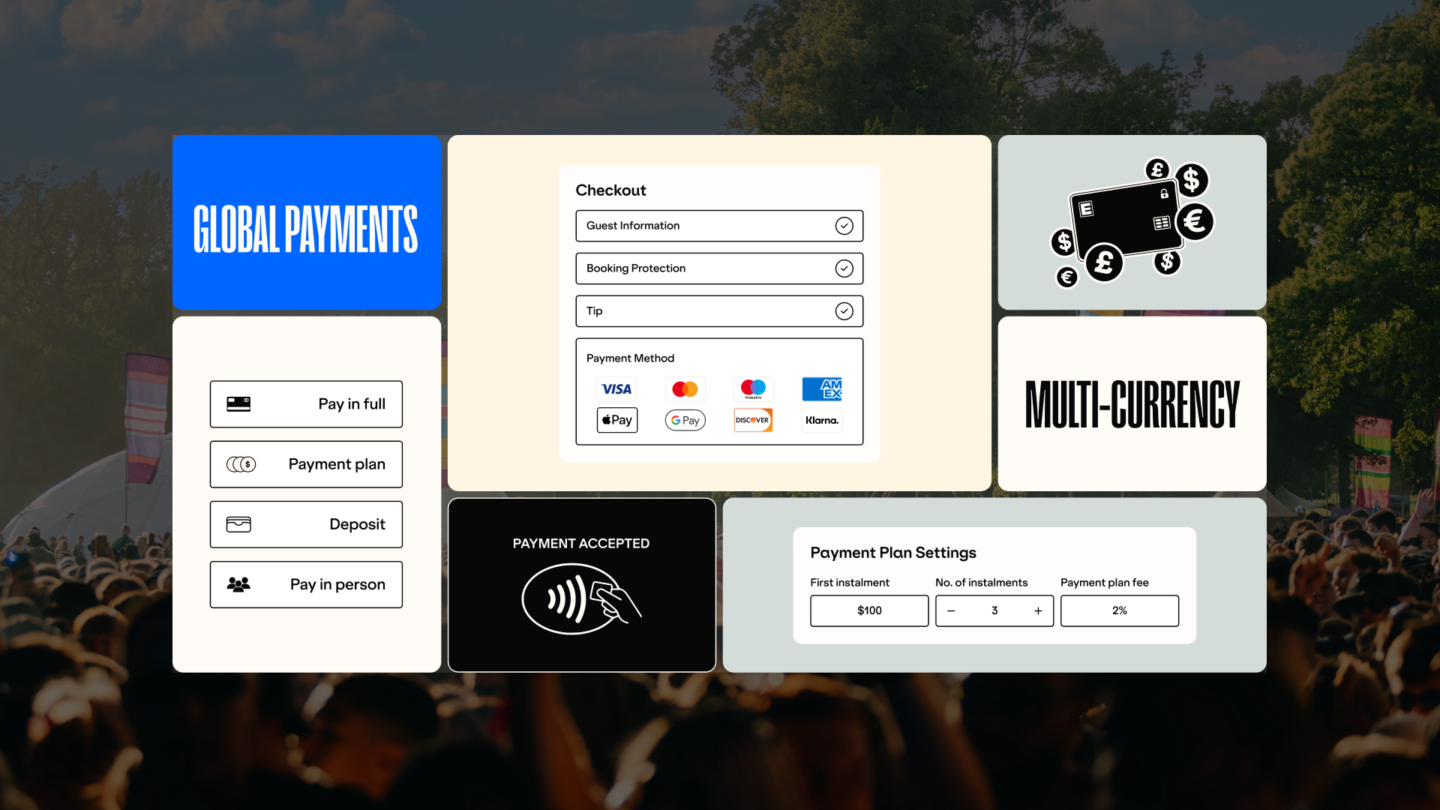

16. 51% of Consumers would be more likely to attend an event if they could pay in installments.

Affordability is now a conversion lever, not just a pricing consideration. Eventbrite’s TRNDS 2025 reporting found 51% of consumers are more likely to attend an event if they can pay in installments, and 56% would use a buy-now-pay-later option for tickets over $100.

Flexible payments only work when they’re native to the booking flow (and cleanly handled across refunds, defaults, upgrades, and add-ons). Easol’s payment stack is built for exactly this kind of reality: deposits, installments, group pay / split payments, and BNPL options like Klarna, all running through a single, first-party checkout on your own domain.

Explore Global Payments Built for High-Value Experiences

Enable a flexible payment stack designed to increase conversion, reduce failed payments, and unlock global demand with group pay, multi-currency support, and custom payment plans.

17. Over 90% of festival tickets are now purchased digitally

Digital is now the default path to purchase for festivals, and mobile is where decisions get made.

This is also where measurable commercial lift shows up when organizers simplify their tech stack. Easol reports that experience businesses moving from multiple disconnected tools to a single unified platform see up to 30% higher conversion, 24% higher basket spend, and approximately 200% ROI within six months. The gains don’t come from heavier marketing, but from removing friction—fewer steps, clearer packaging, and a checkout designed for digital-first behavior.

18. RFID and contactless payments increase per-attendee spend

Festivals that move to RFID/NFC cashless systems commonly report 15–30% higher per-attendee spending, largely because tap-to-pay removes the “small frictions” that suppress impulse purchases (queues, slow authorization, cash handling).

Supporting that behavior shift, Intellitix cites an Eventbrite survey indicating 66% of attendees spend more at events with cashless payment options.

Loyalty & Retention

19. Festivals with sustainability initiatives see higher attendance

Industry research shows that over 60% of festivalgoers say a festival’s environmental impact influences their decision to attend, and events that actively promote eco-friendly initiatives—from waste reduction and reusable cup systems to low-impact transport options—tend to see higher attendance and stronger return intent compared to less proactive peers. This effect is most pronounced among 18–34 year olds.

20. 70% of festivalgoers attend two or more festivals each year — but most organizers can’t recognize them

With 50% attending 2–3 events per year and another 20% attending 5–6 festivals.

When tickets are sold through third-party platforms, much of that behavior becomes invisible. Identity fragments across events, attribution breaks, guest emails are hidden, and behavioral signals (what people browse, abandon, or bundle) remain locked.

More leading festivals are shifting toward owning the guest relationship on a single domain. Easol allows organizers to capture first-party data across the entire journey — discovery, purchase, packaging, and post-event engagement — without handing the most valuable insights to intermediaries.

Operations, Risk & Workforce

21. Labor now accounts for 30–40% of total festival operating costs

Industry benchmarks estimate that staff wages, security, crowd management, and production crew costs typically account for roughly 30–35% of a festival’s total operating budget, particularly for larger multi-day events where significant professional staffing is required. These costs include not just wages, but also compliance, logistical supervision, and seasonal workforce coordination — all of which expand as scale increases.

22. Majority of festival organizers list tech integration and implementation as a top hurdle

Most modern festivals have moved from manual processes to software-driven operations, with the majority using event management software (and many still supplementing with spreadsheets or ad-hoc tools), indicating that festival operators routinely manage multiple tech solutions as a core part of their workflow.

The issue lies in disparate technology solutions that don’t share workflows or data between them. Many festival operators are switching to platforms like Easol for a unified booking management system across every step of the guest experience.

Strategic & Brand Implications

23. Gen Z is 3x more likely to attend live events

Crucially, Gen Z’s engagement doesn’t stop at attendance. They are more likely to:

- Discover events through social and creator-led channels

- Engage with experiences before and after the event (content, community, drops)

- Pay for experiences that feel distinct, intentional, and well-designed

This means festivals aren’t competing with streaming or gaming for Gen Z’s attention, they’re competing with other experiences. The bar is higher, but so is the upside for events that deliver clarity, ease, and emotional payoff across the entire journey.

24. Live Nation continues to post strong revenue growth driven by festivals

Demand remains resilient even in uncertain economic climates.

25. Brand activations at live events drive 4x higher recall than digital ads

Festivals are uniquely effective environments for this because attendees are present, engaged, and receptive. This is why sponsorship dollars continue to flow into festivals: they offer measurable brand impact, not just impressions.

26. Transformative experiences are top of mind for 65% of consumers

According to Eventbrite, among attendees seeking transformative events, 53% say they want experiences that improve their lives, 52% prioritize mental health benefits, and 48% are looking for opportunities to reset or re-energize.

This marks a shift in what audiences expect from festivals and live events. Music remains the draw, but wellbeing, emotional impact, and personal value increasingly influence attendance decisions.

Executive Summary: Why This Matters in 2026

The music festival ecosystem is bigger, more diverse, and more digitally connected than ever. From growing international travel to rising premium spend and hybrid engagement, the industry demands technology that unlocks insights, streamlines operations, and elevates the festival experience — whether your focus is sponsorship monetization, personalized marketing, premium package conversions, or real-time experience orchestration.

Easol’s experience ecosystem, which replaces outdated rigid systems, are uniquely positioned to help organizers unify data, automate engagement at scale, and deliver seamless end-to-end experiences that attendees now expect.