Own Your Checkout: Optimizing Payment Plans for Festivals in 2026

Festivals are no longer an impulse purchase. The festival experience has evolved with add-ons, upgrades, onsite accommodation and travel packages making these a high consideration purchase, often amplified with large groups making the decision together.

This creates a complex purchase for customers which often starts nearly a year before the gates open.

Live Nation recently reported that 40% of fans traveled over 500+ miles for a show this past year, and 6 in 10 of consumers travel for concerts every year.

These longer booking windows and higher spends changes how guests pay and directly affects how fast you sell out and your cash flow.

In 2026, the strongest creators, whether selling single-day tickets or weekend packages will:

- Offer flexible payments, cater for groups and do this without relying solely on 3rd party BNPL providers.

- Use third-party BNPLselectively and deliberately in addition to there own offerings.

- Use payment strategies to increase commitment earlier in the sales cycle, without discounting.

1) Maximize Revenue with first party Payment Plans

The numbers speak for themselves.

1 in 5 UK adults (10.9m people) used BNPL in the 12 months, and in the US it was reported that over 60% of Coachella attendees used payment plans to finance their purchase.

Research backs these trends:

- An experiment found a +20% sales impact when pay-over-time is offered.

- A Stripe A/B test across 1.5M checkouts found up to +14% revenue uplift simply from showing instalment options at checkout.

On Easol, one internationally recognised festival saw 57% of guests book with payment plans contributing to 33% year-on-year revenue growth.

Platforms like Easol are built precisely for this: giving creators full control over deposit size, instalment timing, fees, and cancellation policy. Ensuring you control the entire customer journey and benefit from the commercial upside.

Where third party BNPL providers might charge 6% or more and may have a low acceptance rate for credit.

With first party payment plans, you can offer all guests flexible payments and benefit from the fees your guests would otherwise pay to BNPL firms – by charging a convenience fee on payment plans.

The mechanics are straightforward: a 10,000-capacity festival with a $55 ticket and $5 plan fee at 30% uptake generates $15,000 in incremental, near-pure-margin revenue — before accounting for any conversion uplift from lowering the upfront barrier. At scale, that compounds quickly.

2) When to Use Third-Party BNPL for Festival Ticket Sales

Third-party BNPL is a tactical lever. It’s more expensive and comes with data trade-offs, so it’s best deployed selectively when incremental conversion or risk transfer outweighs the cost.

A clean approach looks like:

Main on-sale window

- Run first-party payment plans: Maximise uptake increasing earlier commitment and speeding up your sell out velocity whilst benefiting from improved margins through owning the customer relationships.

Final 6–8 weeks (if inventory remains)

- Enable third-party BNPL (like Klarna) selectively, you benefit from receiving the full payment upfront whilst your custom benefits from paying post event.

- Use marketplaces tactically to move remaining stock.

3) Designing Payment Plans that Maximize Conversion and Cash Flow

Offering payment plans is expected behavior for consumers, and how you design them can lead to strong financial impact.

The structure of your plan—deposit size, number of instalments, cancellation rules, and group payment mechanics—directly impacts:

- Conversion rate

- Speed of sell-out

- Cash flow timing

- Operational complexity

- Refund and default risk

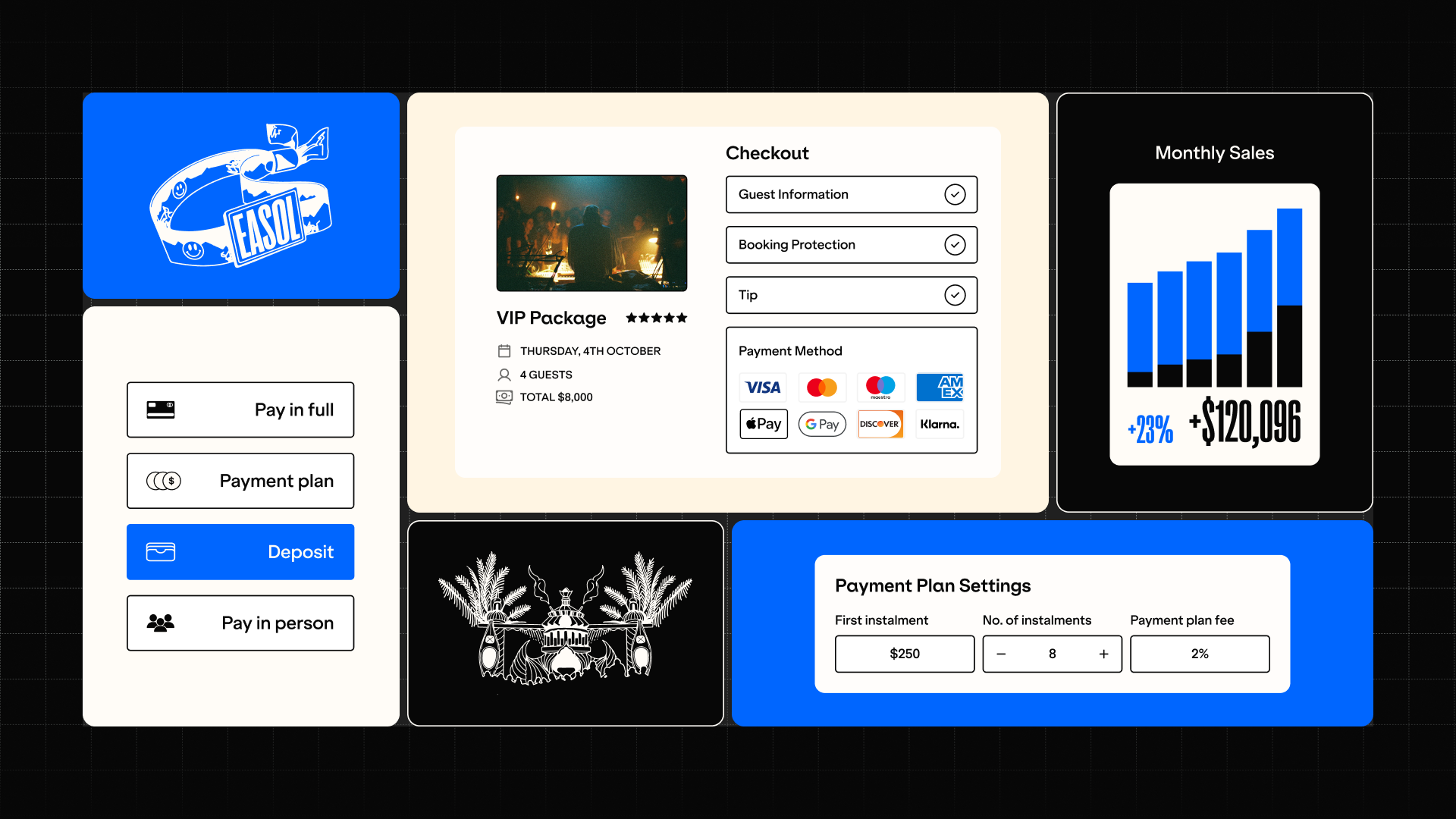

How to set up deposits:

The deposit is the first gate to completing a purchase:

Too high → you reduce accessibility and conversion

Too low → you increase drop-offs, defaults, and operational overhead

A practical range:

- 20–30% deposit → maximises conversion (lower barrier to entry)

- 30–50% deposit → balances conversion with commitment

- 50%+ deposit → prioritises cash flow and reduces default risk

What matters is intent:

- Early on-sale → optimise for conversion (lower deposit)

- Peak demand → optimise for yield and commitment (higher deposit)

- Late cycle → optimise for cash collection (higher deposit or full payment)

Operator rule: Deposits should evolve throughout the sales cycle.

How many installments should a payment plan have?

More instalments increase accessibility, but also complexity. But beyond a point, they stop improving performance.

With Easol handling scheduling, collection, retries, and enforcement automatically, you’re not constrained by operational complexity. You can offer up to 12 instalments if you want.

The question is: what actually converts?

A simple structure works best:

- 2–3 instalments → strong balance of conversion and completion

- 4–6 instalments → useful for higher-ticket experiences where spreading cost unlocks demand

- Beyond that → marginal gains in conversion, with diminishing impact on completion

At that stage, the limiting factor isn’t your system, it’s customer confidence. If the plan feels unclear or overly drawn out, people hesitate or drop off later.

Even with full automation, how payments are structured still matters.

- Monthly schedules tend to feel natural and expected

- Clear, evenly spaced payments increase confidence at checkout

- Tight or irregular schedules can feel like “full payment in disguise”

Easol handles the logic, only showing plans that fit between booking date and event date, so what the customer sees is always viable.

Configuring Group Pay

Group bookings are where payment strategy has the biggest impact. Most travel is inherently social—60% of travellers prefer to travel in groups—and on Easol, the most common group size is two to three people. That turns a single booking into a coordination problem by default.

84% of consumers already use peer-to-peer payments, and expect splitting to be seamless. When it isn’t built into the flow, it gets pushed into messages, spreadsheets, and manual coordination.

Built-in group payment changes that. The booking itself becomes the coordination layer, removing friction at the point where intent is highest.

It also changes behaviour.

On Easol, bookings using Group Pay are significantly more likely to include add-ons—12.3% vs 7.0%. In practice, this reflects how groups buy: higher-value, more considered bookings where packages and extras are part of the decision, not an afterthought.

It also changes what you know. Instead of a single booking tied to one organiser, you capture each guest individually. Creators can see who they are, how they pay, and what they’ve booked.

The strongest setups are designed so that packages are surfaced early, group payment is introduced at the right moment, and the flow adapts to the size and intent of the booking.

Effective group payment design:

- Allow split payments across individuals

- Set clear deadlines for each participant

- Maintain inventory hold rules tied to group completion

- Enable partial commitment without blocking the whole group

Commercial impact:

- Groups are almost 2x as likely to add and upsell or add-on to their purchase

- Consumers purchasing festival tickets are 2.4x as likely to want to pay in installments versus non festival purchases on Easol

- More identifiable customers per booking

Operator rule: The easier it is for groups to pay, the larger the booking you will capture.

4) Putting it all Together

A high-performing payment plan system:

- Lowers the barrier to entry without sacrificing commitment

- Scales across individual and group bookings

- Protects inventory and cash flow through clear rules

- Reduces operational overhead through automation

The goal isn’t maximum flexibility.

It’s controlled flexibility—designed to increase conversion while protecting revenue.

Own the transaction. Own the booking journey end-to-end.

Easol gives festival operators full control over checkout, payments, packages and add-ons in one unified commerce platform.

Launch deposits and installments. Capture incremental payment plan revenue. Optimize cash flow. Keep your customer data.